A Deep Dive into AI Inference Platforms - Part 2

Industry Dynamics and Competitive Landscape in AI Inference

In Part One, we explored the three dominant categories of AI inference platforms—Proprietary Model APIs, Managed Open-Source APIs, and DIY GPU Infrastructure—and broke down their pricing structures, tradeoffs, and target users. But understanding theoretical pricing alone does not fully capture how companies actually make deployment decisions at scale.

In this second part, we shift the focus from price lists to market behavior: how these business models translate into real-world adoption, what drives customer choices, and where the battle lines are forming as the market matures.

We’ve all seen the endless coverage of proprietary model APIs like OpenAI and Anthropic. These platforms have become the default choice for many enterprises and newcomers to AI, thanks to their world-class models and seamless developer experience. But for those building at scale—or looking for more control, customization, and cost savings—the critical decisions are now happening further down the stack. In this section, we focus on the two lesser-covered but fast-emerging categories:

1. Managed API platforms (offering hosted open-source and fine-tuned models)

2. DIY GPU infrastructure platforms (offering bare-metal or lightly managed compute at lower prices).

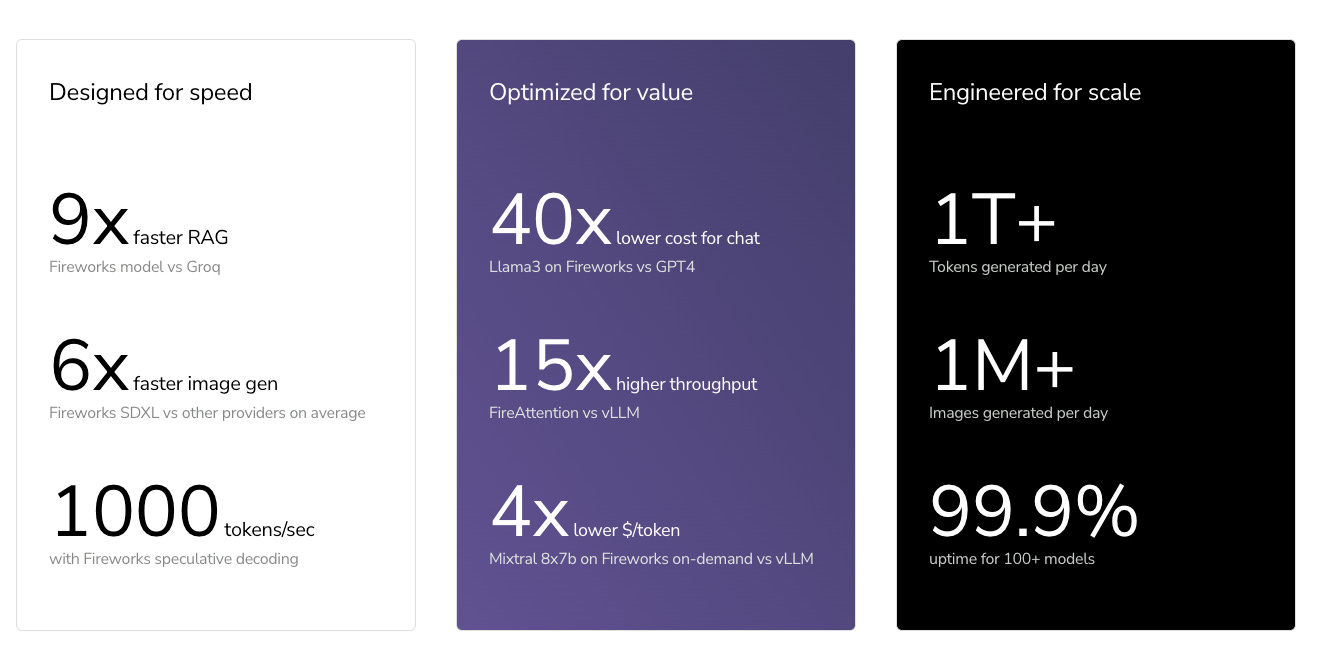

Managed API Platforms: Speed, Efficiency, and a New Layer of Competition

The managed API market has rapidly emerged as a critical middle layer between proprietary model APIs and full DIY GPU infrastructure. Platforms like Together.ai, Fireworks.ai, and others have carved out a strong foothold by serving open-source and fine-tuned models through highly optimized developer APIs. These services strongly appeal to AI-native startups and research teams seeking high performance and low latency without the operational burden of managing their own infrastructure. Providers in this category have prioritized building extremely efficient inference engines with advanced kernel-level optimizations and even custom CUDA kernel development to maximize throughput and minimize latency. Techniques such as speculative decoding, batching, quantization, and fine-grained GPU scheduling have now evolved from experimental innovations to standard production practices, enabling these platforms to deliver lower cost-per-token on popular open-source models. These characteristics make them especially attractive for use cases like large batch inference, conversational agents, and RAG pipelines.

With model weights increasingly commoditized—since many platforms serve the same open-source models such as LLaMA, Mistral, or Mixtral—the competition has shifted heavily toward infrastructure efficiency, orchestration quality, and observability tooling. Providers differentiate by delivering superior inference engine performance, which increases the number of responses per GPU and reduces operating costs. Highly customized inference stacks tuned for prefill and decode efficiency, combined with optimized load balancing and early adoption of multi-model routing, help these platforms attract and retain demanding customers. For example, Together.ai has been consistently praised for its lower latency and stable cost structure, made possible by internal inference engine innovations and proactive GPU resource allocation to avoid noisy neighbor degradation. Fireworks.ai has also led in early adoption of proprietary speculative decoding strategies, kernel-level optimizations, and, notably, running custom inference workloads on AMD chips to reduce hardware costs.

As price and performance differentials continue to narrow, the next wave of competition is increasingly focused on platform experience and developer stickiness. As of 2025, leading providers have begun rolling out integrated fine-tuning pipelines, orchestration frameworks, and early agent frameworks that allow developers to compose smaller specialist models for complex workflows—further blurring the traditional lines between platform categories. These features offer faster setup times and smoother developer onboarding, which is critical for teams migrating off expensive proprietary APIs. The market dynamic closely mirrors the early stages of the cloud infrastructure race, where providers that won key workloads and created high switching costs went on to dominate long-term market share. Looking ahead, platforms with strong internal research capabilities and continuous engineering innovation will be best positioned to lead as this intensely competitive space matures.

DIY GPU Infrastructure: Accessible, Scalable Compute for AI Builders

The DIY GPU infrastructure market has evolved into an essential middle ground for organizations seeking to balance extreme flexibility with cost efficiency. Platforms like RunPod, Lambda Labs, and Vast.ai do not operate their own data centers but instead lease capacity from major colocation providers like Equinix—or even from CoreWeave itself—and package that compute into developer-friendly offerings. This structure allows them to offer GPU access at highly competitive rates, often 30–40% below traditional cloud providers like AWS, Google Cloud, or Azure. These platforms cater primarily to AI-native startups, research labs, and smaller model hosting companies who want to avoid the heavy MLOps and infrastructure lift of traditional GPU clouds but still maintain full control of their model serving and fine-tuning workflows.

What makes these DIY GPU providers unique is the level of abstraction they offer relative to pure infrastructure players like CoreWeave or Nebius. While CoreWeave provides full enterprise-grade infrastructure with extensive Kubernetes and networking customization (typically targeting AI infrastructure teams), platforms like RunPod and Lambda are designed for ease of use, fast setup, and developer self-service. Users can rent GPU instances within minutes using prebuilt containers, Jupyter notebooks, or custom docker environments, without needing deep knowledge of Kubernetes orchestration or networking pipelines. This accessibility has made them particularly popular for workloads like fine-tuning LLaMA models, experimental research training runs, batch scoring tasks, and even early-stage inference deployments.

However, customer feedback has highlighted distinct trade-offs within the category. RunPod has built a reputation for fast setup, transparent pricing, and customizable instance options, but has limitations in terms of multi-region scalability and early access to the latest GPU hardware like H100s. Lambda Labs offers access to cutting-edge NVIDIA architectures and often delivers faster raw training speeds, but customers cite challenges such as variable GPU availability and stricter operational requirements for dataset ingestion. As a result, most teams using these providers adopt a multi-vendor approach to mitigate the risks of price spikes, instance shortages, or service instability.

Despite these operational complexities, the DIY GPU infrastructure market has become a durable niche segment of the AI compute landscape. As generative AI workloads scale rapidly, these platforms remain critical alternatives to both proprietary APIs and fully managed inference services. The value proposition is clear: for teams with sufficient MLOps maturity, the ability to access commodity GPUs at rock-bottom prices, avoid vendor lock-in, and fully own their model pipelines is a powerful incentive. Going forward, customer demands for better international footprint, more consistent availability, and improved customer support will be the key battlegrounds for differentiation.