A Long Meditation on Data Center Cooling Opportunities

A Long Meditation on Data Center Cooling Opportunities

Technologies, Market Players, and Challenges in Data Center Cooling

I’ve been a bit quiet over the last month. We just formed a partnership with Berkeley Sky Computing Lab to serve as a real-world data partner and supply our processed federal transaction and pricing data. This collaboration will help experiment and accelerate LLM batch inference, and we’re thrilled to be part of Matei’s lab’s effort to build batch analytics integrated with LLM technologies.

Anyway, back to data centers. This is a long piece covering many aspects of thoughts that have been on my mind. A few weeks ago, I set out to do a comprehensive analysis of all components of data center infrastructure, only to realize the complexity and technological depth involved. So, taking it one step at a time—unstructured, but moving forward starting from the cooling part.

Microsoft data center near San Antonio TX

As data centers grow rapidly, driven by the surge in AI technologies, the evolution of the infrastructure supporting them—particularly cooling systems—is fascinating. My interest comes from my previous roles as an ex-DC infrastructure/energy economist and an ex-SF industrial equity analyst, and now with my focus on data and AI technologies, data centers are right at the intersection of all of these. I recently visited several data centers in Middle America, both operational and in (phased) development. These investments are reshaping regions that were once off the radar, and I’ve been keeping a close eye on this shift.

AI workloads require far more processing power, which means they generate way more heat than traditional operations. As data centers expand, managing this heat becomes crucial. Without proper cooling systems, data centers can’t run efficiently and risk hardware failures, which could limit their ability to support AI-driven innovations.

Cooling systems play a key role in keeping data centers at optimal temperatures. If heat isn’t handled well, the whole facility could face performance issues or even hardware damage. Cooling technologies range from traditional air-cooled systems to more advanced options like liquid cooling and, more recently, immersion cooling. These innovations are designed to handle the higher heat densities that modern AI workloads create, making sure data centers can keep up with today’s tech demands. With AI pushing power densities higher and higher, we’re seeing a slow but steady shift toward liquid and immersion cooling. I’ll dive into those density calculations and why the industry is moving in that direction shortly.

Market Players and Investable Universe

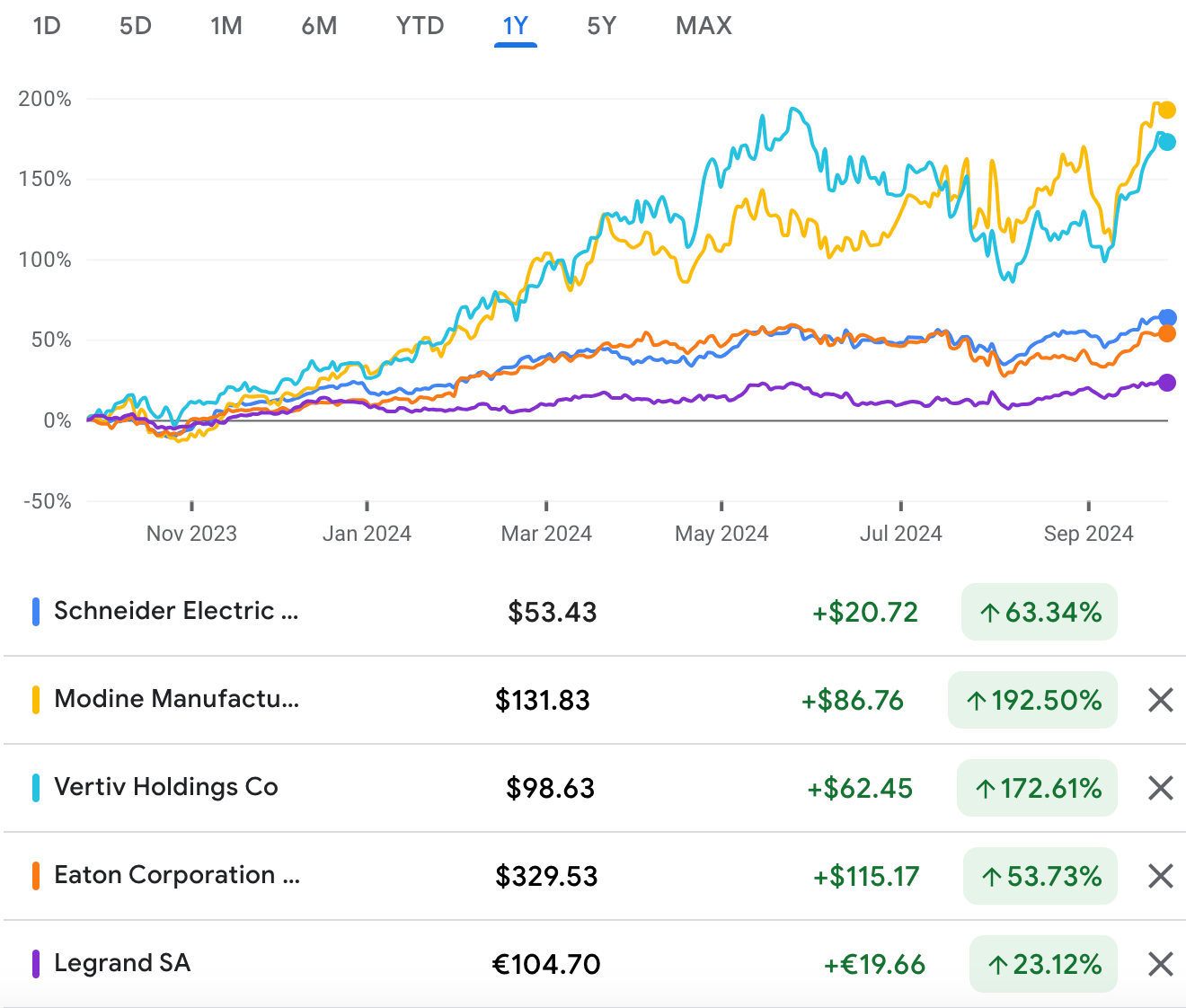

The data center cooling market, especially for public equity investment, is a relatively small universe, with the top five players controlling over 50% of the market. Ranked by size, these include Schneider Electric, Vertiv, Eaton, Legrand, and Modine. Among them, Modine and Vertiv are closely tied to AI growth and NVIDIA’s stock performance due to their focus on advanced cooling solutions for high-density AI workloads.

While Modine and Vertiv are more pure players, their stocks have acted as proxies for NVIDIA’s success. However, their expertise differs. Modine, through its Airedale division, is known for its strong air-based cooling systems and is transitioning towards liquid cooling. Vertiv, on the other hand, offers a broader range of solutions, including chilled water systems and innovative technologies like EconoPhase for smaller data centers. As AI demand rises, their cooling systems are essential, making them critical to data center infrastructure.

In contrast, Schneider Electric, Legrand, and Eaton, although they occupy a larger share of the data center cooling market, are less correlated with NVIDIA and AI trends due to their diversified portfolios, which focus on energy management, power distribution, and digital infrastructure across multiple sectors. Although they play key roles in data center operations, their broader focus dilutes their direct connection to the AI-specific cooling needs that Modine and Vertiv target.

Top 5 data center cooling technology supplier stock performance

On Modine

I find Modine fascinating—how a small, old company has strategically transformed into an AI data center cooling pure player over the last decade, all thanks to a smart acquisition. Who doesn’t love a great makeover and growth story?

Modine Manufacturing, though the smallest public player in the space, has become a near-perfect proxy for NVIDIA in equity growth. Founded in 1916 in Racine, Wisconsin, Modine was primarily focused on HVAC and industrial cooling for most of its history. The turning point came in 2005 when it acquired Airedale, a U.K.-based specialist in data center cooling. Airedale brought not just technological expertise but also a solid market presence in the FLAP region (Frankfurt, London, Amsterdam, Paris) with a 25-30% market share in the U.K.

This $38 million acquisition (only half of Airedale’s sale at the time!) allowed Modine to pivot just as AI and cloud computing were driving demand for more advanced cooling solutions. Modine is Known for producing high-quality, long-lasting products (chillers and air handling units that last 15-20 years), Modine has built a solid reputation in both the U.S. and Europe. Its data center business hit $294 million in sales in 2024—a 69% YoY growth, with an EBITDA margin of 18.3%. And they’re guiding for 80-90% growth for the year.

However, there are some concerns. While Modine is still strong in air cooling, the risk is that it might lose market share in the next 4-5 years unless it pivots to liquid cooling, which is quickly becoming the standard for AI-driven data centers. Schneider Electric, in contrast, is perceived to be better positioned for long-term success with a broader range of solutions and a strong focus on sustainability, particularly in liquid cooling by some.

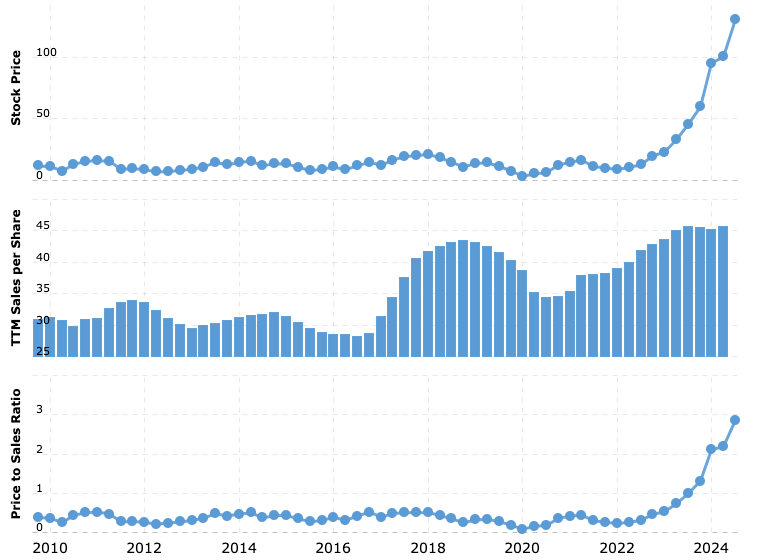

Also, when it comes to price, Modine and Vertiv aren’t exactly cheap. Their overall revenue growth is solid but not mind-blowing—around 12-20% from 2022 to 2023. However, what’s really wild is the multiple expansion. Both companies’ price-to-sales (P/S) ratios have surged by 10x since 2022. You can’t argue with market sentiment.

Modine stock price, sales per share, and P/S ratio since 2010

Notes on Different Cooling Technologies

I’ve discussed several different technologies in data center cooling. AI workloads are significantly increasing the power density of data centers. Previously, hyper-scale data centers operated at around 10 to 20 kilowatts per rack or square meter. However, with the rise of AI and high-performance computing tasks, this demand is expected to rise dramatically to 50 kilowatts or more per rack, with some applications already reaching 100 kilowatts per square meter. The industry is shifting toward liquid cooling and immersion cooling, which are more efficient for handling such high heat loads but still rely on systems to manage heat rejection efficiently.

1. Traditional Air Cooling: This method remains dominant, especially for lower-density workloads. It involves using air to remove heat from servers and relies heavily on chillers, fans, and compressors to cool the air and recirculate it. However, as data centers become denser, this method becomes less effective, particularly for high-performance computing tasks like AI workloads.

2. Free Cooling: A growing trend, free cooling utilizes outside air or natural cooling methods to reduce energy consumption. This method eliminates the need for mechanical cooling (compressors) when external temperatures allow it. It’s seen as a more energy-efficient solution, especially in cooler climates.

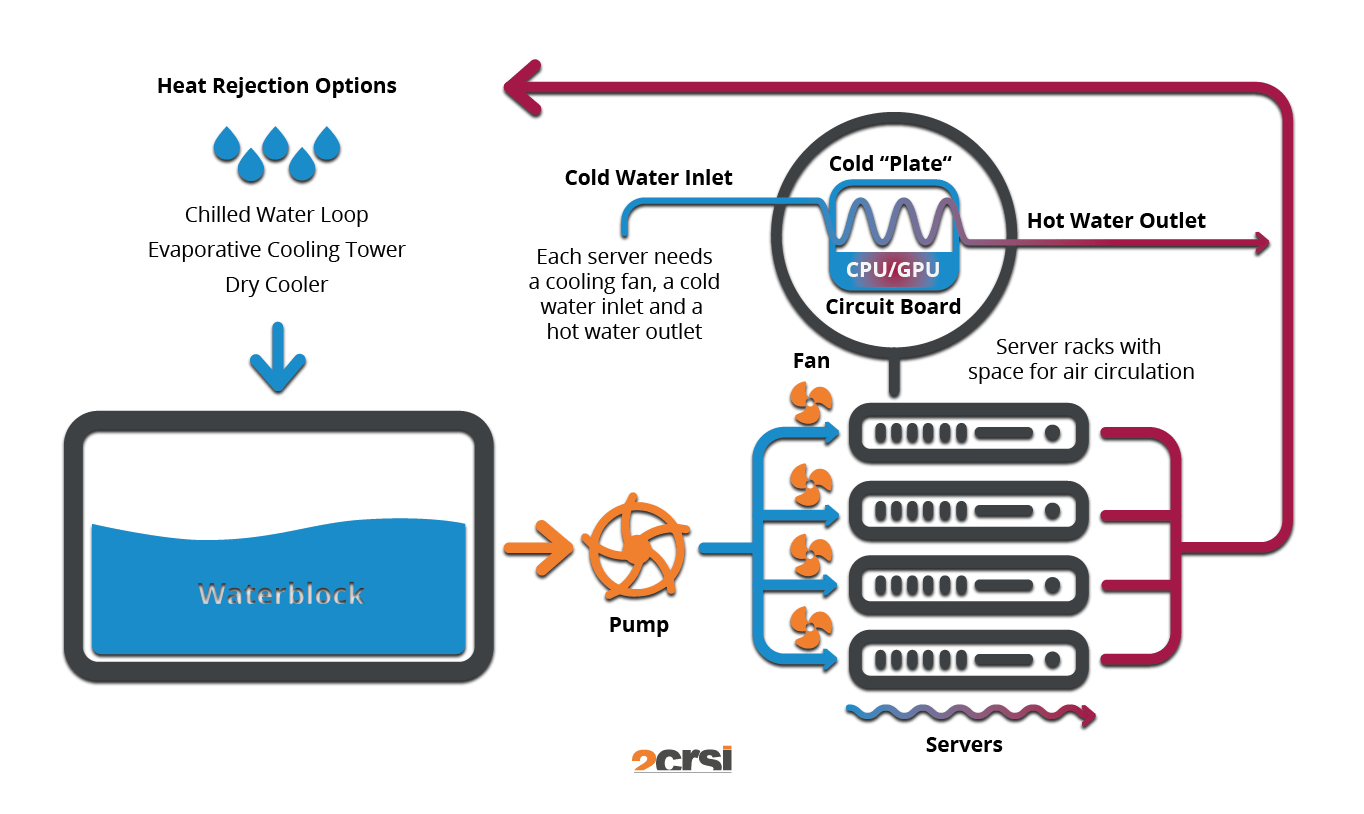

3. Liquid Cooling: Liquid cooling commonly uses direct-to-chip cooling, where liquid flows through tubes and passes over a plate placed directly on the processor or GPU. This method efficiently draws heat away from the component, keeping it cool even under heavy workloads.

4. Immersion Cooling: Immersion cooling goes a step further by fully submerging entire servers or hardware components in a non-conductive liquid. This special fluid absorbs heat without damaging the electronics, making it even more efficient for high-performance computing environments like AI-driven data centers, where the heat output is significantly higher.

5. Heat Rejection: Heat rejection is the process of removing excess heat generated by servers and electronic components to maintain optimal performance and prevent overheating. In traditional air cooling, heat is expelled through chillers, fans, and compressors. In liquid and immersion cooling systems, the heat absorbed by the cooling liquid must be removed using heat exchangers, pumps, and cooling towers, which dissipate the heat to the outside environment. As data centers evolve toward higher densities, the ability to efficiently manage and reject heat becomes crucial to maintaining performance and preventing system overloads.

Why Liquid and Immersion Cooling Won’t Happen Overnight

What direct liquid cooling looks like

The data center industry is gradually shifting from air cooling to liquid cooling, driven by the rising heat demands of AI workloads. While liquid cooling has historically been used in niche markets like high-performance computing (HPC), it’s becoming more mainstream, especially with direct-to-chip cooling as air cooling reaches its limits. However, retrofitting existing data centers for liquid cooling poses significant challenges, requiring upgrades like Coolant Distribution Units (CDUs) and new piping systems. Large players like Vertiv and Schneider Electric are investing heavily in these technologies to integrate liquid and air cooling solutions. Meanwhile, smaller innovators like Asetek and Green Revolution Cooling are advancing liquid cooling, but larger incumbents have the advantage due to their global service networks and ability to scale. While liquid cooling is gaining traction, it will likely coexist with air cooling in the near future.

Immersion cooling is increasingly being discussed as a solution for managing the rising heat densities in modern data centers, particularly with AI-driven workloads. Immersion cooling submerges entire servers or hardware in a non-conductive liquid, offering a more efficient way to handle these demands. However, the transition to immersion cooling will be slow because air-cooled systems currently dominate 95% of the market and,again, are designed to last 25-30 years. This means existing data centers will continue relying on air cooling for some time, with upgrades happening gradually.

As immersion cooling gains traction, cooling manufacturers are evolving their products, focusing on heat rejection rather than traditional mechanical cooling components. This shift allows new technologies to be adopted while older air-cooled systems remain in place for lower-density workloads and legacy data centers.

What immersion cooling looks like, from immersion cooling specialty company Submer

Immersion cooling is rapidly emerging as a critical solution for managing the increasing heat densities in modern data centers, particularly those driven by AI workloads. This technology is gradually replacing traditional air cooling, which is becoming less effective for high-performance tasks as data center heat loads continue to rise. While immersion cooling offers a more efficient way to handle these demands, the transition will be slow, as traditional air-cooled systems dominate 95% of the current market and are designed to last 25-30 years. As a result, existing data centers will continue to rely on air cooling for some time, with upgrades occurring gradually. However, as the shift towards immersion cooling progresses, cooling manufacturers are evolving their products, focusing on heat rejection rather than mechanical cooling, which aligns with the needs of immersion systems. This evolution ensures that new technologies can be adopted while older air-cooled infrastructures remain in operation for lower-density applications and legacy systems.

Startups and Early-Stage Innovation

The private data center cooling companies like Munters, Stulz, Nortek Air Solutions (air cooling), Asetek, ZutaCore, CoolIT Systems (liquid cooling), and Submer, Green Revolution Cooling (GRC), Iceotope, and LiquidStack (immersion cooling) have a more niche, regional focus compared to larger public players like Vertiv and Modine. These smaller firms often concentrate on specific regions such as Europe (Stulz, Iceotope, Submer) or North America (Nortek, GRC, CoolIT), though many are expanding globally. They focus on specialized cooling technologies like precision liquid and immersion cooling, catering to high-density workloads and edge computing, while larger public companies have broader global operations and serve a wider range of industries beyond high-performance computing and AI-driven data centers. Vertiv and Modine, for example, not only cover cooling but also power infrastructure and have deep service networks worldwide, allowing them to scale more rapidly, unlike smaller private companies that are still growing and mainly serve hyperscalers, HPC centers, and cloud providers in specialized markets.

Also, connecting this with what we monitor in federal innovation awards, the DoD and DoE have both awarded multiple grants for data center cooling technologies over the last few years. Here are some notable companies that have received Federal awards in this area, along with their locations and what they specialize in.

1. Flexnode Inc

• Location: Bethesda, MD

• Focus: Flexnode is developing Prefab Modular Liquid-Cooled Micro Data Centers, which are designed to meet the cooling needs of edge computing environments. Their solutions involve the use of liquid cooling to efficiently manage heat in micro data centers, allowing for enhanced performance in high-density computing environments, especially in smaller, localized facilities.

2. Impact Cooling LLC

• Location: Birmingham, AL

• Focus: Impact Cooling works on developing High-Density Cooling Systems for Ultra-Low PUE (Power Usage Effectiveness) Data Centers. Their technology aims to improve energy efficiency in data centers, focusing on reducing the overall energy consumption needed to cool high-density servers, a critical challenge for large-scale data center operations. They aim to push the limits of cooling technology to handle the increasing power demands of modern data centers, especially in AI and cloud environments.

3. Advanced Cooling Technologies Inc

• Location: Lancaster, PA

• Focus: Advanced Cooling Technologies (ACT) is focused on Electrically Isolated Hybrid Two-Phase Cooling Systems for use in data centers. Their systems are specifically designed to cool advanced electronic components, such as RF power devices, which are essential for next-generation data center technology. By enhancing heat management for high-performance electronics, ACT is improving the reliability and efficiency of data centers.

4. Green Revolution Cooling, Inc.

• Location: Austin, TX.

• Focus: Green Revolution Cooling (GRC) is a leader in submersion cooling systems, where data center hardware is submerged in a non-conductive cooling liquid. This method offers superior energy conservation and heat dissipation compared to traditional air-cooled methods, making it particularly effective for modern, high-density data centers that support AI and other demanding computing tasks. GRC’s technology helps data centers lower their cooling costs and improve energy efficiency.

Hyperscalers: Still Very Very Hard for Startups and Why

The data center cooling sector is an exciting space, driven by rapid advancements in technology and the growing need to manage heat loads from AI and cloud workloads. Innovations like liquid cooling, immersion cooling, and hybrid systems are making data centers more efficient and sustainable. However, the success of these technologies relies heavily on robust distribution channels.

In a market where most cooling components—compressors, fans, and pumps—are similar, the real differentiation lies in a company’s ability to provide superior service and maintain reliable supply chains. Hyperscalers like Microsoft and Google typically enter into long-term contracts (three to five years) with cooling suppliers after extensive due diligence. This 2 to 2.5-year due diligence period includes evaluating suppliers, assessing reliability, ensuring supply chain stability, and securing necessary permits before finalizing these contracts. The focus is more on reliability and the ability to meet large-scale demands consistently, rather than just technological superiority. For instance, Microsoft relies almost exclusively on Vertiv in Northern Europe, while other regions may favor Schneider Electric.

Hyperscalers also divide contracts regionally to ensure competitive pricing and service efficiency. Companies like Vertiv, Schneider, and Modine succeed because of their established relationships and their ability to quickly respond to large enterprise demands. Without strong distribution networks, even the most innovative cooling solutions struggle to gain traction in this competitive market, making it particularly challenging for startups to break in.

And that’s it for now :)